ASML: Service Is The Business

Wall Street prices the $350M systems. I'm buying the 30-year tail at 70% margins

For: growth-tilted / total-return investors

Horizon: 5+ years

Position: BUY at ~$1,065

Data: as of 1/29/2026

The Mismatch

ASML sits around ~$1,065 — and the long-term story is still intact. But the stock doesn’t trade on “long-term stories.” It trades on orders (net bookings) and guidance tone.

ASML is the monopoly toll booth for advanced lithography. That’s not up for debate. The mismatch is this: investors treat a monopoly like it can’t wobble — but the quarterly path is still governed by bookings, customer timing, and mix.

The market prices the destination. The stock prices the order book.

The Call

Thesis: ASML is essential infrastructure for leading-edge compute — but even essential infrastructure can deliver ugly quarters. At $1,065, I’m a buyer for 5+ years, but I’m not blind to bookings risk.

What the Company Actually Does

ASML doesn’t make chips. It makes the machines that decide who can make chips.

ASML sells lithography systems — DUV and EUV — plus upgrades and services. EUV is the gatekeeper for leading-edge nodes, and ASML is effectively the only supplier.

High-NA EUV is the next step. It’s a real commercial ramp — but early ramps aren’t margin miracles. They’re execution tests.

What’s Breaking

The secular story is real. The quarterly path is still a knife fight.

Bookings are lumpy by nature. One quarter doesn’t prove “new regime.” Two or three do.

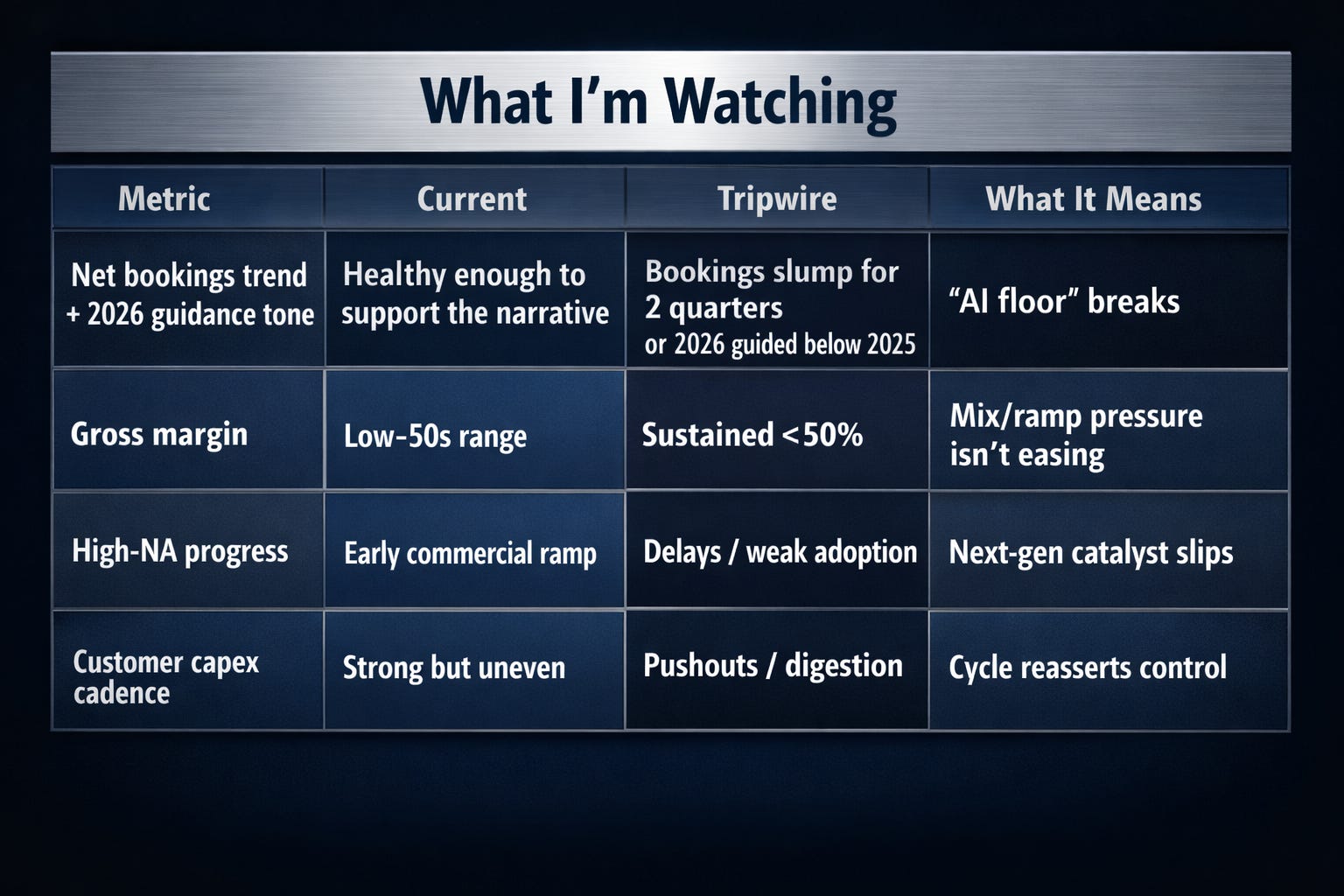

Margins aren’t the story — until they are. Gross margin has lived in the low-50s range recently. New ramps can be dilutive early.

Customer timing is the hidden lever. The biggest fabs decide cadence; they can pull forward, then pause.

China/mix sensitivity matters. Shifts in where demand comes from can change the feel of a quarter fast.

Crowded longs don’t unwind slowly. They gap.

The Gap (Consensus vs Reality)

Street view: AI keeps the machine humming. The monopoly prints.

My view: The monopoly is real — but the stock trades on the order book. You can have the right 5-year story and still eat a nasty 6-month drawdown if bookings blink.

The Street models a glide path. This business delivers surges and stalls.

Where the Returns Came From

Great companies still get you — not on the business, but on the entry price.

Over a 3–5 year window, ASML’s returns typically come from two places:

Earnings growth (the real engine): shipments, service growth, mix, and operating leverage over time.

Multiple expansion / contraction (the mood swing): the market pays up in “sure thing” periods and compresses fast when bookings scare people.

Translation: at $1,065, your upside case is earnings compounding plus a market that stays willing to pay for it. Your downside case is a bookings wobble that compresses the multiple even if the business remains strong.

How It Actually Trades (The Machine)

ASML trades on two words: bookings and guidance.

Marginal buyer: AI/semicapex funds, ETFs, quality-growth managers

Embedded narrative: Monopoly + AI = “can’t lose”

Price mechanics: earnings, bookings, guidance tone, customer capex plans, High-NA milestones

Capital return math:

Dividend: ASML pays a dividend (income is not the point here, but it’s real).

Buybacks: ASML does repurchase shares — supportive, but not the core thesis. The core thesis is reinvestment + demand durability.

ASML returns cash — but it’s a reinvestment machine first.

How It Handles News

Strong bookings / confident guide = the stock rips.

Any hint of order digestion = the stock sells first, asks questions later.

How It Plays Out

Bull path:

Bookings stay firm, 2026 tone stays constructive, High-NA ramps without drama, service grows, earnings compound.

Bear path:

Bookings wobble, customers digest spend, and the stock reprices hard because the multiple was renting perfection.

What It’s Worth (3–5 Years Out)

ASML will still be critical infrastructure in 3–5 years. The debate is price vs. path.

At $1,065, I’m buying the business — and accepting that the stock can still punch you in the face if bookings blink.

What the Tape Says

The tape can be confident and still be wrong for a quarter or two.

Price action reflects belief in the secular AI/compute buildout. That’s fine — but the tape does not override bookings.

Who Owns It and Why It Matters

Institutions and thematic funds own it because it’s the cleanest “compute picks-and-shovels” expression in public markets.

That’s a feature… until it’s a risk.

How I’d Actually Build the Position

Starter: meaningful (because this is a 5+ year call)

Add: on bookings strength + steady 2026 tone

Size up: after a volatility event proves the “floor” is real

Price Zones (What I Do When)

Buy zone: here (~$1,065) for a 5+ year horizon

Add zone: meaningful pullbacks if bookings stay intact

Trim zone: if the narrative turns perfect and bookings don’t confirm it

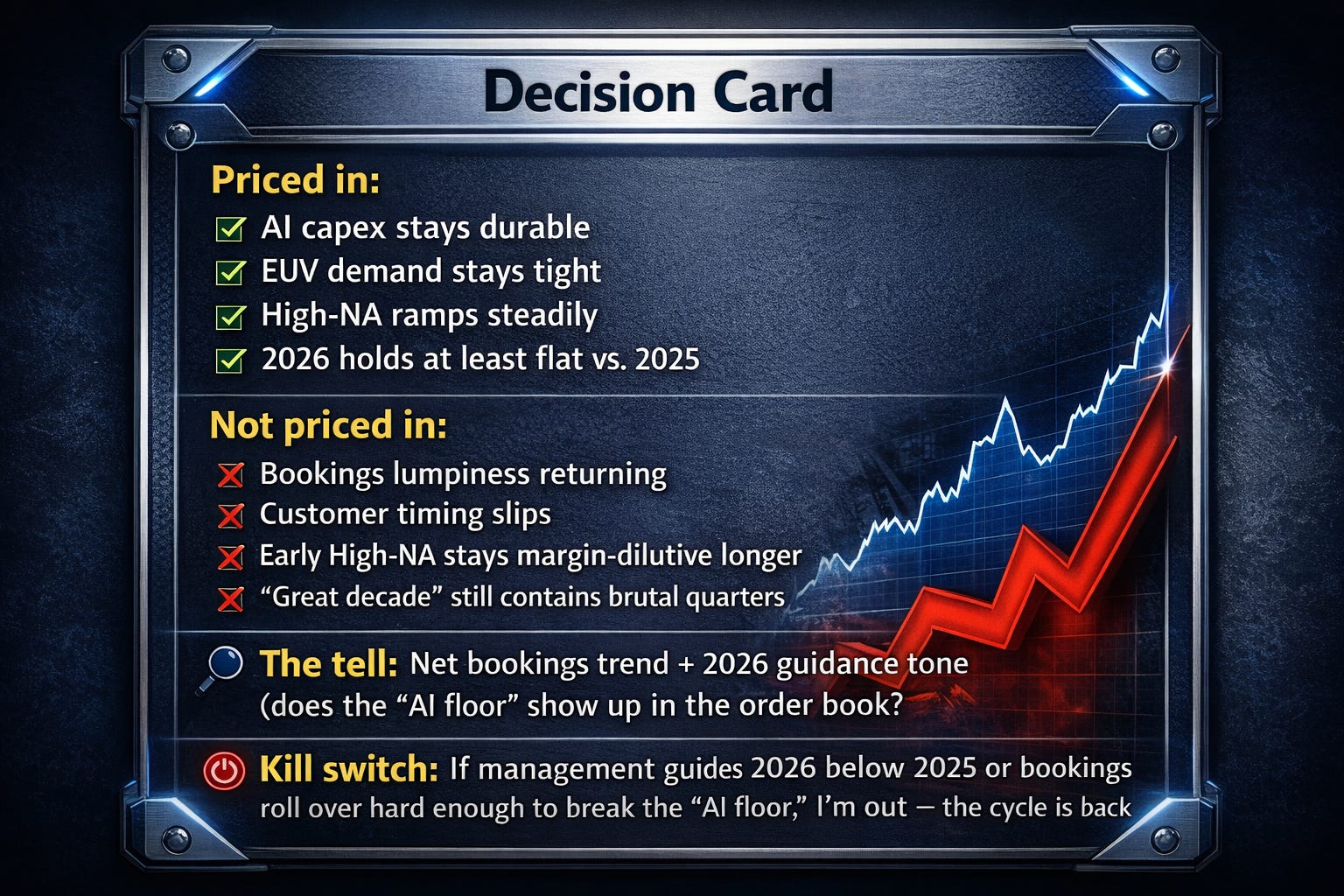

What Would Flip Me

Bookings deterioration that signals a real digestion year

2026 revenue guided below 2025 (cycle wins)

High-NA adoption slipping meaningfully from “commercial ramp” expectations

The Line (Kill Switch)

If the order book cracks, the multiple has no reason to stay elevated.

If management guides 2026 below 2025 — I’m out.

If bookings slide hard enough to break the “AI floor” narrative — I’m out.

Bottom Line

BUY at $1,222 (as of 1/5/2026) for growth-tilted, total-return investors with a 5+ year horizon.

ASML is essential infrastructure — but it’s still a stock that lives and dies on bookings + guidance tone. I’m willing to own that volatility because the monopoly is real. I’m not willing to ignore the order book.

Disclaimer

This content is for informational and educational purposes only — not financial advice. Do your own due diligence before investing. Nothing here is a recommendation to buy or sell any security.