Microsoft (MSFT): The AI Empire Under Siege

Beat on every line. Margins fine. Regulators loading the cannons.

Microsoft just posted a quarter that would make any CFO weep with joy. Wall Street yawned. Regulators smiled. Revenue hit $77.7B, up 18% and beating estimates by $2.4B. Azure rocketed 40% (cc), Microsoft Cloud $49.1B (up 26%), and EPS $4.13 against $3.67 expected. Guidance? Q2 revenue pegged at $79.5-80.6B, implying another 14-16% pop.

The stock dipped 1% post-earnings.

Affiliate Disclosure: I’m a FAST Graphs affiliate. If you click a FAST Graphs link in this post and choose to subscribe, I may receive a small commission. It doesn’t change your price, and all opinions are my own.

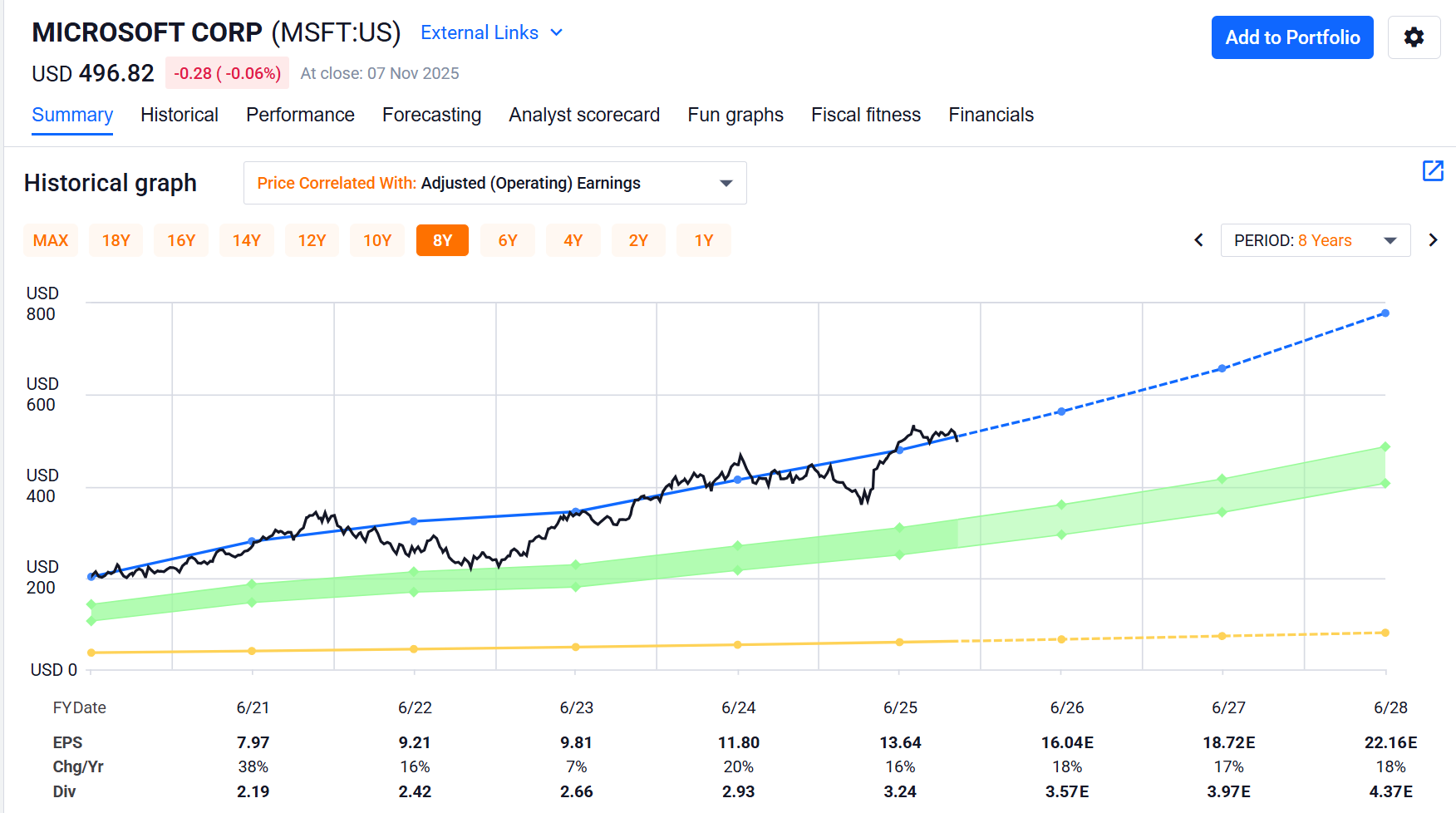

Price (solid) vs adjusted earnings (dashed). Price outran earnings through ’24–’25—multiple stretch that’s vulnerable to any Azure slowdown or regulatory hit.

Here’s why: A fresh antitrust class-action lawsuit—filed Oct 13, 2025 in N.D. Cal.—slammed Microsoft over its OpenAI deal, alleging it stifles competition and locks out rivals. The FTC probe is heating up, OpenAI tensions are boiling (they’re eyeing a contract review), and EU regulators are sniffing around data dominance—OpenAI itself flagged concerns to the European Commission on cloud/AI competition. The empire that swallowed Activision and bet billions on AI is now defending its crown—while burning a record $34.9B in Q1 CapEx to stay ahead of demand.

Cloud revenue soared, but Microsoft 365 Commercial cloud growth ticked +17%. China direct revenue is just 1.5% of total, but Azure is indirectly exposed via multinationals’ China operations amid tightening US export curbs. The moat is vast. The war chest overflows. But the growth story justifying 36× earnings? It’s under cannon fire from regulators.

📊 The Scorecard

Metric Grade Reality Check Moat A+ Office + Azure lock-in is ironclad Cash Flow A $78B TTM FCF, endless dividend fuel Growth A- 18% revenue pop, Azure at 40% Valuation C 36× earnings for 12% expansion Risk Profile C Antitrust suits, CapEx bloat Innovation A Copilot + OpenAI lead the AI charge

🔥 Heat Map: Where’s the Fire?

Category Status Watch For Azure/Cloud Strong Capacity constraints ease; >42% YoY (cc) for two quarters = blowout OpenAI Partnership Watch Tensions resolve; FTC greenlight = unlock Antitrust Risk Lawsuit settlements; breakup risk fades China Exposure Watch Tariff hikes; Azure growth dip >5% = red alert Valuation Watch Compress to 30×; sub-$450 entry point

The Bull Case: Cloud + AI = Unstoppable Scale

Bulls have a point—Azure’s 40% surge is no fluke, fueled by AI tailwinds and enterprise stickiness. Copilot’s a beast: Nearly 70% of the Fortune 500 use Microsoft 365 Copilot, the Copilot family has surpassed ~150M monthly active users, and 80% of new GitHub devs use Copilot in week one. Add AI revenue run-rate >$10B (FY25), and it’s easy to see Microsoft Cloud hitting $100B+ annually by 2027. The OpenAI tie-up cements MSFT as AI plumbing for the Fortune 500 (>85% using Microsoft AI overall). Q2 guidance signals sustained 14%+ growth, and that $78B FCF war chest funds FY26 CapEx growth > FY25 (Q1 already ~$35B) without breaking a sweat—bulls argue at 40% Azure growth, this spend turns accretive by FY27, juicing margins back to 42%.

Refinements like Azure AI Studio and integrated Copilot in Office? They deepen the ecosystem moat—evolution into the AI OS, not just a side hustle. If regulators back off and Azure hits 45%+, bulls could push fair value to $600+ on 18% sustained growth.

My Take: Execution Meets the Regulators

Microsoft builds empires like no one else. But with antitrust suits piling, nearly a third of growth now rides on AI hype, not organic cloud wins. Legacy segments like Windows are mature, replacement cycles steady at 3-4 years.

Azure’s 40% growth looks dominant—until you stack it against peers.

Google Cloud’s at ~35% YoY from ~13% share; AWS grew ~18% in Q3 ’25, holding ~29% (Azure ~20%).

GOOGL trades at ~23× forward P/E with that cloud acceleration;

AMZN ~29–34× on half the growth. Microsoft’s premium is the narrative, not the numbers—yet. A 2–3-point share slip could shave ~$50 off my target. Supply constraints persist through at least June 2026 (FY26 end), per IR.

At 36× forward earnings—rich even vs. peers like Adobe (~14–15×), Salesforce (~22×), and ServiceNow (~45–55×) on similar or slower growth—Microsoft needs 15%+ annual revenue growth through 2030 to support the multiple.

Value Math: Fair Value $450

Using conservative assumptions:

12% revenue growth through 2027

Op margin steady at 40%

9% cost of equity

Terminal growth 4%

Affiliate Disclosure: I’m a FAST Graphs affiliate. If you click a FAST Graphs link in this post and choose to subscribe, I may receive a small commission. It doesn’t change your price, and all opinions are my own.

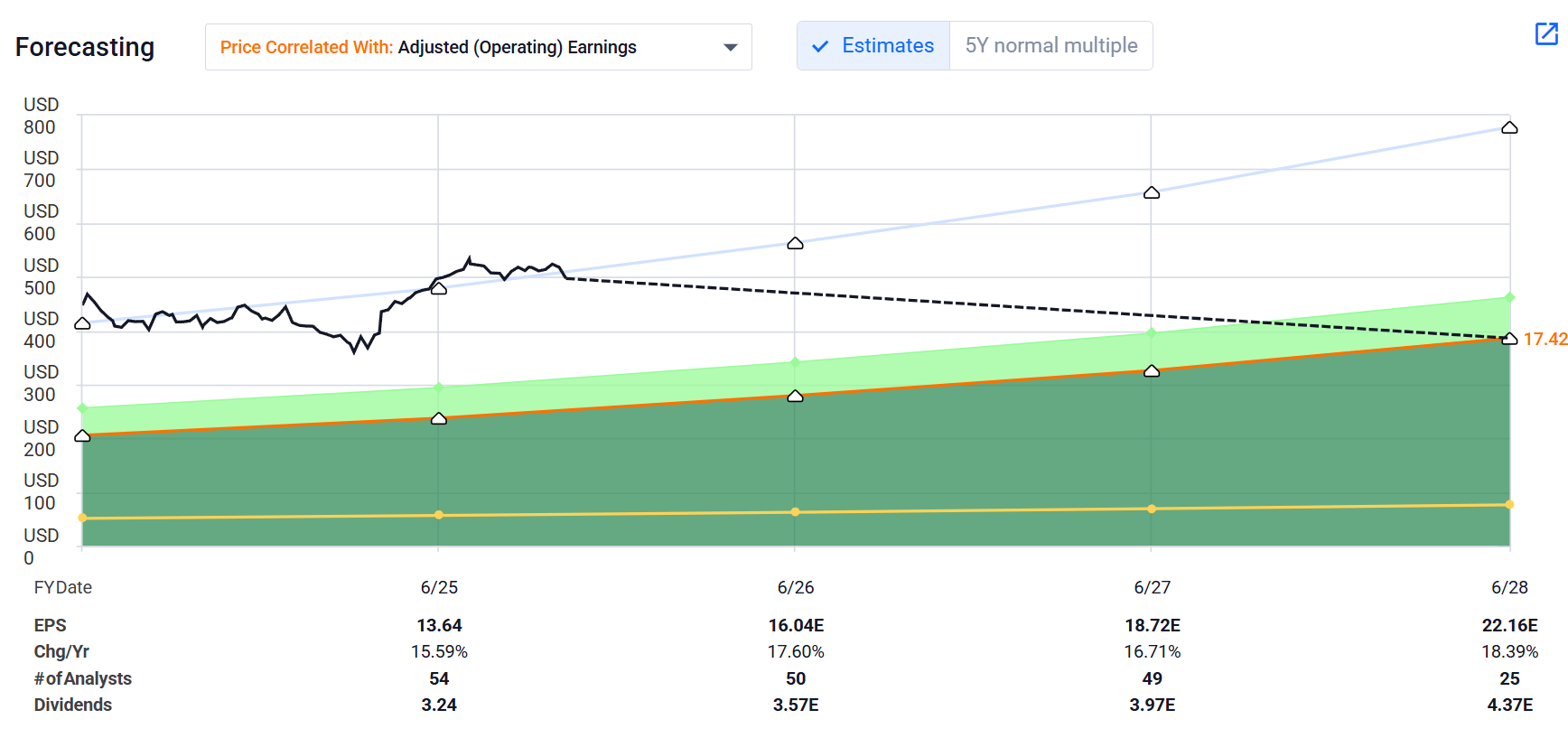

Consensus EPS steps up ~16–18%/yr; a 15×–18× band implies fair value below today’s 36× narrative. My $450 DCF lines up with this band.

DCF spits out $450/share—a 9% trim from current levels. That’s where the AI premium gets stress-tested against red tape.

For sensitivity: A higher CoE (10%) or lower TGR (3%) pressures the target further—see the quick table below.

Scenario CoE TGR Fair Value Base 9% 4% $450 Stress 10% 3% $380 Optimistic 8% 5% $520

Disclosure: Long MSFT position (8% of portfolio—material enough to watch closely, not bet the farm).

What Would Change My Mind

I’d turn more bullish if:

Azure growth accelerates past 45% for two consecutive quarters

Antitrust suits settle favorably (no breakup, exclusivity intact)

China exposure stabilizes with zero rev impact from tariffs

Valuation compresses to 30× or below on accelerating FCF

Until then, I’m holding my long with no adds—watching the siege unfold.

The Earnings Reaction & Risk Stack

Q1 catalyst (Oct 29): Smashed EPS ($4.13 vs $3.67), revenue $77.7B topped $75.3B est. Shares slipped 1% after hours—the market’s pricing flawless AI bets amid lawsuit headlines. As of November 8, 2025, shares flat near $500, as OpenAI drama lingers without fresh catalysts.

Key risks stacking up:

Antitrust escalation—OpenAI class action could force divestitures, EU probe threatens data deals

CapEx explosion with FY26 growth > FY25 (Q1 already $34.9B)—binge today, margin squeeze tomorrow if Azure slips below 35%, compressing ops to 38% by 2027 as AI data center ROI lags 18-24 months

China tariffs (1.5% direct rev, but Azure vulnerable via multinational ops)

AI bubble pop if Copilot adoption stalls post-hype

My Kill Switch

I exit if:

Azure growth dips below 30% for two quarters

FCF falls under $70B TTM (CapEx overrun kills)

Antitrust forces OpenAI unwind (partnership implodes)

Multiple stretches past 40× (hype fully detached from delivery)

Affiliate Disclosure: I’m a FAST Graphs affiliate. If you click a FAST Graphs link in this post and choose to subscribe, I may receive a small commission. It doesn’t change your price, and all opinions are my own.

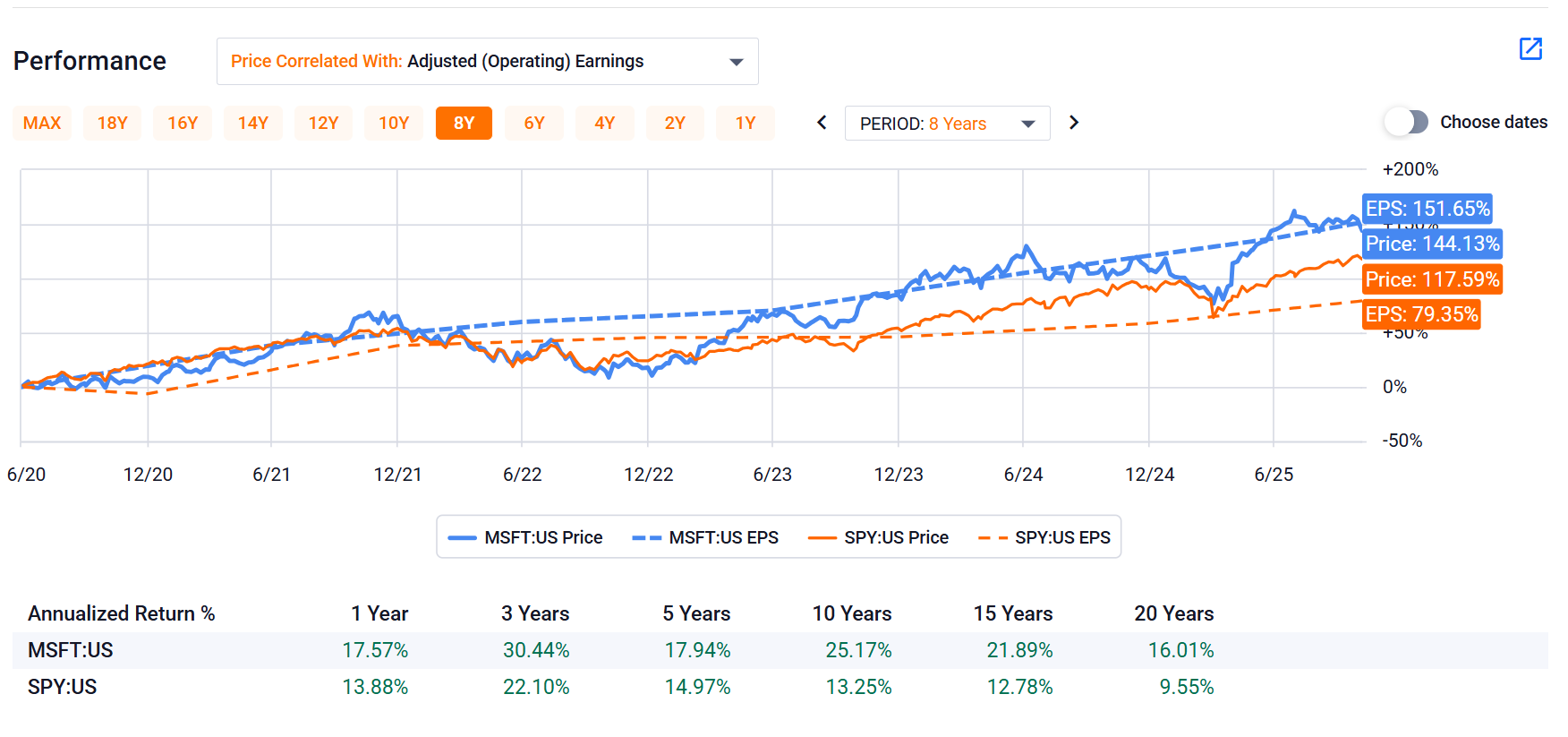

MSFT still outperforms the S&P 500. Moat intact; risk is paying peak narrative—returns compress if AI momentum or growth cools.

Bottom Line

Microsoft pumps $78B in annual FCF, deploys it via $20B+ dividends and buybacks. Vast moat, AI frontrunner, balance sheet like Fort Knox.

But the empire’s under siege. OpenAI lawsuits mounting. CapEx frenzy. China trade winds shifting.

Timeless builder. Relentless scaler. Priced like the AI singularity’s here—but regulators say not so fast.

What To Watch

Price Target: $450 | As of Nov 8: $500 | Downside: 9%

Azure capacity vs. demand—supply constraints through mid-2026?

OpenAI antitrust updates—settlement timeline or escalation?

Q2 Copilot adoption metrics—real enterprise pull or pilot fluff?

Margin trajectory—can op margins hold 40% amid escalating CapEx?

Disagree with my $450 target? Tell me why in the comments—I’m here to stress-test the thesis, not defend it.

DISCLAIMER

This publication reflects my personal research and investment process. Nothing here should be interpreted as financial, investment, tax, or legal advice, or as a recommendation to buy or sell any security.

Markets involve risk, including the possibility of permanent loss of capital. My views may change as new information appears, and I may buy, sell, or hold securities mentioned at any time without notice.

For full details, see the Disclosure & Disclaimer page.