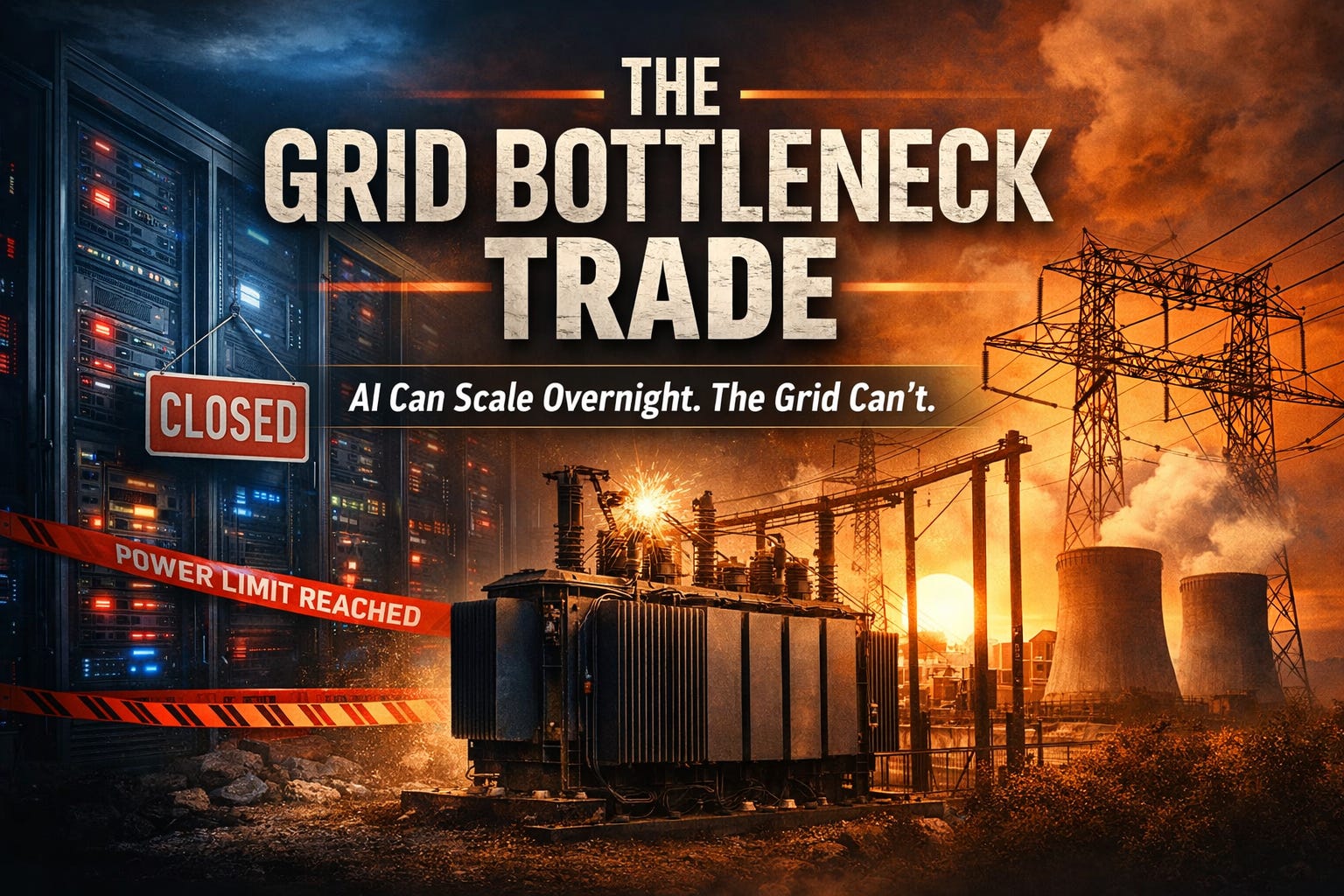

The Grid Bottleneck Trade

AI Can Scale Overnight. The Grid Can’t.

AI can scale in months. The electric grid scales in years. That gap is the trade.

A $2 billion data center can be “done” and still be dead on arrival.

The servers are racked. The fiber is lit. The cooling systems hum.

Then it hits the part nobody can brute-force: the substation can’t take the load, the transformer isn’t available, or the interconnection study comes back with a timeline that reads like a joke.

The Thesis

Power delivery—not chips—becomes the constraint.

We keep talking about AI like it’s software. Like it lives in the cloud and multiplies on command.

It doesn’t.

AI is an industrial build-out wearing a hoodie.

The Mismatch

Data centers can be planned, financed, and built fast.

The grid can’t.

The grid is land, permits, equipment lead times, and regulators. It is a physical network with hard limits and weak links.

And AI demand doesn’t arrive politely. It arrives in lumpy chunks—a single campus can pull city-level load from day one. Utilities and regulators are built for steady growth, not sudden step-changes.

So the constraint shifts from:

“Can we build the compute?”

to

“Can we feed the compute?”

Where the Bottleneck Actually Lives

Most people picture the grid as “wires.” That’s incomplete.

The real choke points are the unsexy parts and the slow approvals:

substations

step-down transformers

switchgear and breakers

protection systems

right-of-way

interconnection queues

Transformers are the cleanest example of why this is sticky.

They aren’t a quick reorder. They’re customized, long-lead, and supply chains tighten fast when everyone upgrades at once.

Even when generation exists on paper, delivery can be constrained exactly where the load shows up.

This is why the grid bottleneck trade is not a one-quarter story.

It’s a multi-year capex cycle with friction built in.

The Trade, in Plain English

When a system hits a bottleneck, money pools around whoever owns and expands that bottleneck.

In the grid world, that often means:

regulated utilities and transmission owners (rate base grows, returns are allowed)

the builders and suppliers behind the upgrade cycle (transformers, switchgear, cable, conductors)

If you want a concrete picture, imagine a fast-growing region where data centers are flooding in. The local utility announces a multi-year transmission and substation buildout to support load growth. Regulators may fight over pacing and cost controls, but the direction stays the same.

Because the alternative is shortages, constraints, and political pain.

Scarcity forces spending.

This is old-school investing logic.

AI is the gold rush.

The grid is the railroad.

The Second-Order Effects

Once power becomes the constraint, behavior changes everywhere.

1) Data centers start paying to move faster.

They stop waiting and start writing checks—funding interconnection upgrades and substation work because the cost of delay is bigger than the cost of steel.

2) Geography shifts.

“Cheap land and tax incentives” lose to “power-rich and buildable.” The map of where digital infrastructure lives gets redrawn by grid capacity, not just real estate.

3) Onsite generation comes back.

Not because it’s trendy. Because it’s firm.

If the grid can’t deliver enough, you bring your own: turbines, microgrids, storage, demand-response contracts.

You don’t do it because it’s perfect.

You do it because downtime is unacceptable.

4) Utilities can re-rate in the narrative.

They stop looking like sleepy bond proxies and start looking like gatekeepers of a new industrial cycle.

That doesn’t mean “up only.” It means the conversation changes.

Risks You Can’t Ignore

This trade has teeth, but it isn’t clean.

Regulators can turn hostile if ratepayers feel like they’re subsidizing billionaire data centers. That can slow approvals, squeeze allowed returns, or force cost-sharing.

Infrastructure overruns are real, especially when equipment lead times stretch and everyone is bidding for the same components.

AI capex is cyclical. If hyperscalers pause, projects get deferred. The grid build remains durable, but the urgency premium can cool.

A clean way to frame it:

Grid modernization is durable.

AI-driven load growth is the variable.

The Punchline

The future doesn’t run on hype.

It runs on electricity.

And right now, the bottleneck isn’t the model. It’s the transformer, the substation, the interconnection approval, and the line capacity that actually delivers power to the rack.

The grid bottleneck trade is betting on the people who can deliver what AI can’t scale without.

Disclaimer

This is not financial advice. I’m not telling you to buy or sell anything. I’m laying out a theme and the logic behind it like I would if we were talking it through at the kitchen table. If you act on any of it, do your own work, assume you can be wrong, and size it accordingly.