The Problem With CrowdStrike Isn’t the Business. It’s the Price.

If retention holds, the premium holds. If it slips, it breaks.

For:

Growth-tilted investors

Horizon: 3–5 years — not a trade

Everyone’s buying the AI story.

No one’s pricing the execution risk.

Post-2024 outage, retention is the real test.

Retention is the fulcrum. Everything else is commentary.

Core Thesis

CRWD is a speculative growth play at today’s price — priced for perfection in a competitive cybersecurity market.

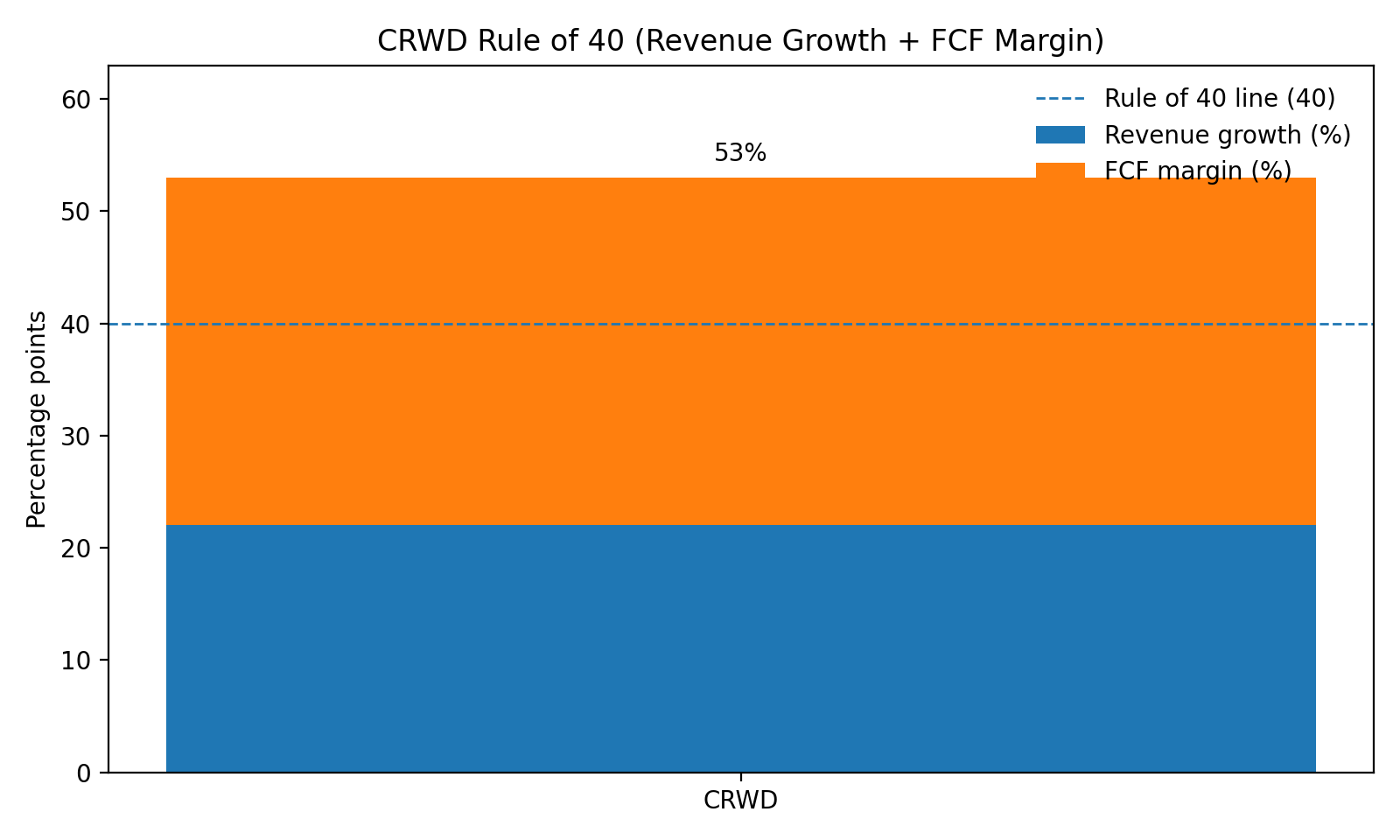

Rule of 40 at ~53% (22% growth + 31% FCF margin) supports the story, but the multiple assumes no slips.

“The engine is real. The price assumes it never sputters.”

This isn’t “is CrowdStrike good?”

It’s “can CrowdStrike be flawless from here?”

Business & Fundamentals (What the Company Is)

CrowdStrike sells cloud-native cybersecurity platforms, primarily through its Falcon subscription service, with segments in endpoint protection (core), cloud security, identity, and threat intelligence.

Revenue is $4.57B TTM, growing at ~22% YoY — decelerating from 30%+ peaks but sustained by module adoption and customer expansion.

Gross margin ~74%. Operating margin negative at -5.6% but trending toward breakeven on scale; R&D heavy at 20%+ of revenue.

Free cash flow $1.42B TTM, FCF margin ~31%, with FCF per share rising despite mild dilution.

Balance sheet: net cash ~$4B, light leverage.

Capital allocation: growth-first with R&D/capex priority; $1B buyback program active but modest at today’s price; no dividend.

Valuation snapshot: Forward P/E 106x, EV/FCF ~83x, FCF yield ~1.2%; rich vs peers (Palo Alto ~60x forward P/E).

Great business doesn’t save you from a great price.

Red Flags / What’s Changing

July 2024 global outage: caused massive IT disruptions, led to lawsuits, potential churn. Retention is the real test.

Valuation extreme: 106x forward P/E leaves no margin for growth misses or margin delays.

Margin pressure: operating losses persist despite scale; competition could cap expansion.

Customer concentration: ~20% of ARR from top 10 clients; loss of one hits hard.

Churn rising: net retention rate ~115%, down from 120%+ pre-outage; watch for further slips.

Competition: Microsoft, Palo Alto integrating AI faster, eroding moat.

High-multiple stocks don’t die from disasters. They die from disappointment.

Expectations vs Reality (Consensus Check)

Street view: consensus prices in 22% revenue growth, margins to mid-teens by 2027, 30%+ EPS CAGR; buckets as AI-growth leader.

My view: growth slows to 15–20% on larger base and competition; margins improve slower post-outage; consensus ignores retention risk.

Consensus is a straight line. Reality has teeth.

Return Attribution (Where Did the Money Come From?)

5-year total return ~112% (Dec 31, 2020 close ~$222 to Dec 18, 2025 ~$470, no dividends).

The point: returns came from execution + staying expensive.

Your earlier framing had a math issue: forward P/E going ~150x to ~106x isn’t multiple expansion — it’s compression. The premium didn’t vanish. It just got less forgiving.

The market already paid you once for the story. Now it wants proof.

Price Mechanics (The Machine)

Marginal buyer: growth funds and AI-themed ETFs; crowded with ~74% institutional, discretionary on narrative strength.

Buyback math: At $470, $1B buys ~2.1M shares — under ~1% of the share count. Less effective than at $300.

Embedded narrative: 106x forward prices “AI-powered cybersecurity dominance.” If adoption or retention falters, multiple compresses.

Caption: “This is the premium you’re renting.”

Dependency: ~60% of revenue from endpoint protection segment (per filings/your framing); at ~83x EV/FCF, a lot of value is tied to one category staying dominant.

Reflexivity: high valuation aids stock comp for talent and M&A currency; loop weakens if price drops below $400.

When the multiple is the product, the customer is sentiment.

The Dashboard (What I’m Monitoring)

MetricCurrentTripwireWhat It MeansARR growth YoY22%<15% for 2QCore expansion narrative breaks, signals saturation.Operating margin-5.6%No improvement to positive in 4QScale thesis fails, FCF growth stalls.Module adoption rate~8 per customer<7 averageCross-sell engine slows, revenue per user drops.Net retention rate115%<110% for 2QChurn accelerating, post-outage damage persists.Institutional ownership74%<65%Crowding unwinds, passive selling pressure.Forward P/E multiple106x>120x or <80xThesis revisit if detached from fundamentals.

If you only watch one thing: retention. Everything else is downstream.

Catalysts & Timeline

Bull path (6–24 months):

Retention rebounds >120% in 2 quarters → narrative reinforcement, multiple stretches.

New AI module launches exceed 20% adoption in 12 months → revenue surprise.

M&A in identity space next year → expanded moat.

Bear path (6–24 months):

Earnings miss on churn in 1 quarter → 20% price correction.

Regulatory fines from 2024 outage materialize → trust erosion.

Competitor gains share visibly in 18 months → growth deceleration.

It doesn’t need a recession. It needs one “clean” quarter that isn’t clean.

Tactical Read

Stock ~17% off 52-week high of $567, up 58% YTD but flat last 6 months post-volatility; momentum fading, traders waiting for retention data.

Waiting is poison at 100x.

Positioning & Flows

CRWD sits in the growth bucket and is crowded. If the market rotates away from growth, the stock can bleed even if fundamentals hold.

When you’re priced for perfection, “fine” is failure.

Strategic View & Value Math (3–5 Years)

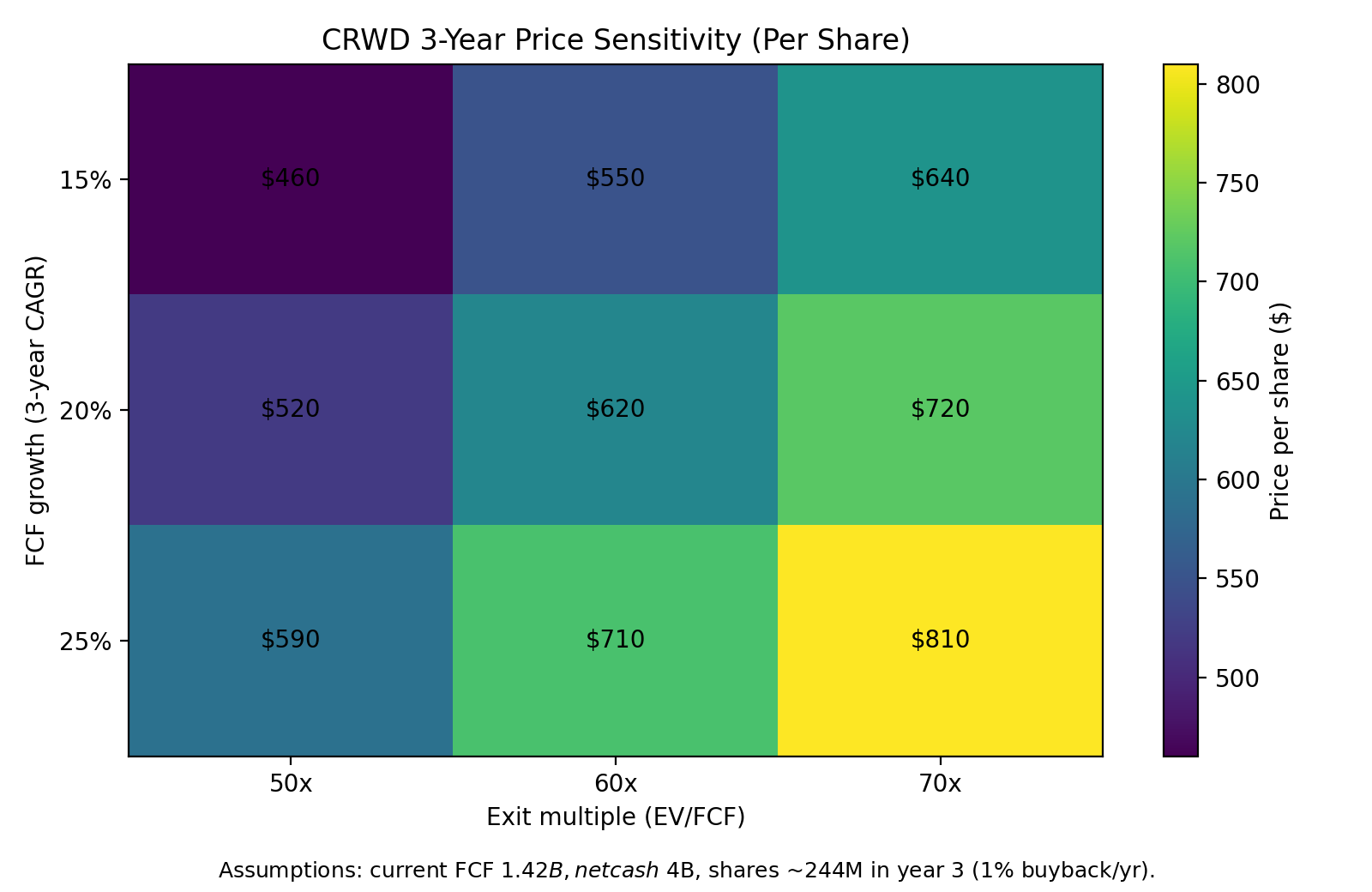

Current FCF: $1.42B

Assumed FCF growth: 20–25% annually over 3 years

Exit multiple: 50–70x FCF

Shares outstanding today: 252M

Assumed buyback pace: 1% annually → ~244M shares in 3 years

Net cash: ~$4B

Pick your assumptions — the math is here.

Pick your assumptions — the math is here

Today’s price ~$470 is basically bear math unless retention rebounds.

Your upside is growth. Your downside is trust.

Decision Framework

Buy zone: $350–$400 (where you’re finally paid for the risk).

Hold zone: $400–$500 — current position, no action.

Trim zone: >$550 or if net retention <110%.

Time horizon: 36 months for thesis to play out.

At $470, you’re not buying a bargain. You’re renting a premium.

What Would Change My Mind

If net retention tops 120% for 2Q, outage damage over — raise growth assumption 5%.

If operating margin hits positive in 2Q, scale ahead — bump target 15%.

If institutional drops below 65% for 6 months, add crowding risk — wider safety margin.

If major outage recurs, cut fair value 20% on churn spike.

If endpoint revenue share drops below 50%, diversification working — more bullish.

If Rule of 40 falls below 40, growth story cracks — revisit bear case.

The narrative protects the multiple… until it doesn’t.

Kill Switch

If ARR growth <10% for 2Q, I’m out — engine stalled.

If another global outage hits, I’m out — trust irreparable.

If forward P/E >120x without earnings beat, I’m out — bubble territory.

If net cash flips to net debt >$2B, I’m out — leverage risk.

No hedging. No “reassess.” Just out.

Final Take / Investor’s Lens

If you’re a growth-tilted investor, CRWD fits for AI upside despite risks. For conservative types, it’s a mismatch on volatility.

For my own portfolio, at ~$470 this is a watchlist, sized as speculation.

I’d rather miss the next leg than pay for unproven perfection.

The best growth investors don’t avoid risk. They refuse to overpay for it.

If this is how you like to think about stocks — filings first, cash over stories, clear kill switches — that’s what I do here every week.

I’m building a small group of investors who care more about coverage math, downside risk, and opportunity cost than hype and victory laps. We read the filings, stress-test the story, and keep each other honest.

If you want to be part of that, hit Subscribe to Phaetrix Investing and stay in the loop for the next deep dive.

Disclaimer

This publication reflects my personal research and investment process. Nothing here should be interpreted as financial, investment, tax, or legal advice, or as a recommendation to buy or sell any security.

Markets involve risk, including the possibility of permanent loss of capital. My views may change as new information appears, and I may buy, sell, or hold securities mentioned at any time without notice.

For full details, see the Disclosure & Disclaimer page.

I currently have PANW. I believe this sector is in for a tailwind in the next few years. But very pricey.