Waste Management at 29x Earnings: Great Business, Dangerous Price

Record margins, strong cash generation, and disciplined pricing — the question is whether the premium multiple has already priced it all in.

WM is expensive for a reason.

Margins are at record highs. Pricing is disciplined. Free cash flow is growing fast.

The problem is that great businesses can still become bad stocks when the price already assumes the good news keeps coming.

Get this wrong and you do not lose money fast. You lose it slowly by owning a great company that goes nowhere while capital compounds somewhere else.

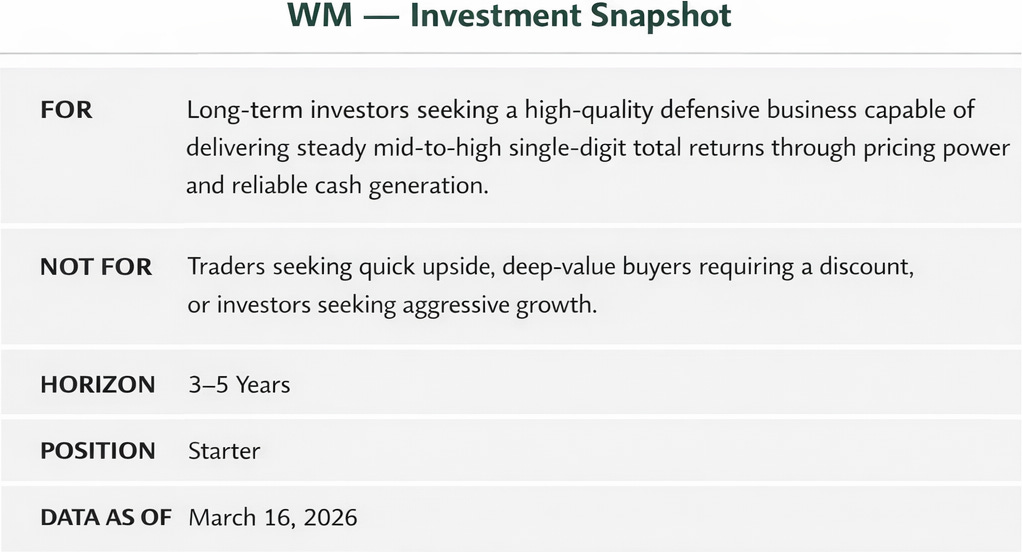

SNAPSHOT

WHY NOW

Waste Management just posted the kind of numbers premium stocks are supposed to post: record efficiency, expanding margins, and guidance for nearly 30 percent free-cash-flow growth in 2026.

The problem is that stocks trading near 29x earnings do not get rewarded for simply performing well.

They get rewarded only if performance remains exceptional.

SETUP

Waste Management is North America’s largest solid waste services company, earning the bulk of its profit by collecting, transporting, and disposing of commercial and municipal waste while also operating landfills, transfer stations, recycling facilities, and a growing healthcare solutions business through the recent Stericycle integration. What is genuinely working today is exceptional cost discipline paired with core price realization that has driven adjusted operating EBITDA margins to 31.3 percent in the fourth quarter and set the stage for further gains in 2026.

MISMATCH

The mismatch is not the business.

It is the price being paid for the business.

At roughly 29x forward earnings, the market is pricing recent execution as though it is the new permanent baseline.

That leaves little room for softer volumes, integration friction, margin normalization, or even merely “good” rather than exceptional execution.

BASE RATE

High-quality defensive compounders in mature industries with strong pricing power and cost discipline tend to deliver respectable but not spectacular long-term returns when purchased at premium valuations, with the most common failure mode being years of sideways performance or multiple compression when growth moderates and patience wears thin.

DECISION CARD (PRICED IN)

The market already believes WM will continue delivering steady pricing, incremental margin expansion, and strong free-cash-flow generation that supports growing dividends and buybacks. It is paying a premium today for a business with limited downside volatility and high earnings quality in almost any reasonable economic backdrop.

DECISION CARD (NOT PRICED IN)

What remains underweighted is how durable the recent structural cost improvements really are and whether Stericycle synergies and sustainability investments can compound into modestly higher margins without requiring perfect execution. The market is also giving limited credit to the possibility that free-cash-flow conversion stays above 46 percent and funds meaningful capital return even if organic volume growth stays modest. If that durability proves real, the multiple holds. If it doesn’t, the premium disappears faster than the business deteriorates.

BASE CASE

If disciplined pricing and cost optimization remain the primary driver, WM generates mid-to-high single-digit annual total returns from current levels through a combination of earnings growth, dividend increases, and share repurchases while the premium multiple is largely maintained because of the business’s defensive characteristics.

BUSINESS RISK

Stericycle integration delivers fewer synergies than expected or encounters operational friction. Pricing power weakens or volumes decline more than anticipated in a softer economy.

STOCK RISK

The stock does not need bad news to fall.

It may only need results that are less perfect than the market expects.

BULL MECHANICS

Proof arrives when adjusted operating EBITDA margins sustainably hold above 31 percent and free cash flow hits or exceeds the $3.8 billion midpoint guidance for multiple quarters. When that proof materializes, the stock can continue to compound as fundamentals support the current valuation and modest multiple stability, with capital returns providing the majority of the total return rather than dramatic rerating.

NEXT

The tape has shown resilience near recent highs with modest pullbacks on macro noise, and a clean break above $245 would confirm continued buyer conviction. Long-only institutions focused on quality and dividends are the primary drivers right now, with the next catalyst being the Q1 2026 earnings report in late April that should give an early read on 2026 execution.

ALTERNATIVE

Republic Services (RSG) offers a comparable defensive profile with slightly less integration risk and a marginally cleaner valuation setup right now, but WM still edges it out for investors who prioritize greater scale in healthcare waste and sustainability projects.

PLAYBOOK

I would play this as a Starter position by adding gradually on weakness toward the low $220s, with a maximum position size of around 4-5 percent of the portfolio. Flip conditions are simple: add on continued margin strength and raised guidance, reduce or exit if integration issues surface or if the stock breaks below $210 with conviction.

WRONG IF

The core assumption is that the structural cost gains and pricing discipline will sustain margins and cash flow growth sufficient to support the premium valuation. Evidence that would prove it false is meaningful margin contraction or missed free-cash-flow targets in the next two to three quarters, with a time tripwire of the next two earnings reports to avoid turning the position into dead money.

Kill switch

The setup changes if margins stop expanding while the premium multiple remains elevated.

The clean signal would be adjusted operating EBITDA margins falling back below 31 percent, free cash flow missing the $3.8 billion midpoint target, or Stericycle integration failing to deliver the expected synergies over the next two to three quarters.

If that happens, the market stops viewing WM as a premium defensive compounder and starts treating it like a mature waste operator priced too aggressively for slowing growth.

BOTTOM LINE

Waste Management remains one of the best businesses in the market.

The issue is not quality.

It is that the current price assumes that quality remains nearly flawless.

Starter only.

Own it for durability if you want.

Do not mistake durability for bargain pricing.

SUBSCRIBE

Subscribers get every new framework-driven stock post and one additional piece each week, plus occasional updates when a thesis materially changes. You also get the full archive of decision documents so you can track how these calls evolve over time.

DISCLAIMER

This publication reflects my personal research and investment process. Nothing here should be interpreted as financial, investment, tax, or legal advice, or as a recommendation to buy or sell any security.

Markets involve risk, including the possibility of permanent loss of capital. My views may change as new information appears, and I may buy, sell, or hold securities mentioned at any time without notice.

For full details, see the Disclosure & Disclaimer page.

I looked into this one as well. Matter fact I looked at all the waste refuse companies. I went and physically talked to people at Casella. I ultimately settled on them. Smaller company in the northeast. I live here and see them first hand. We have a lot of small garbage private companies around that just can’t compete. Casella buys them out. They are growing by small town, small business acquisition after another. Use to be from Bangor to I think mass. Now they stretch from Bangor to New Jersey moving out towards Niagara. The price is better especially after its most recent drop. Might be worth doing your own math on of course. Everyone else to me was just too expensive.

Love this one. I got in on WM at around $227 which I know is a bit high. Will add more when it’s get cheaper. But a long term non-AI hold for me and felt it was needed in my portfolio.