TAIWAN SEMICONDUCTOR (TSM): Record Highs Meet the Margin Reality Check

Flawless execution is assumed. Margin stability must be proven.

For: growth-tilted / total-return investors

Horizon: 5+ years

Position: BUY at $1,065 (current)

Data: as of 12/24/2025

The Mismatch

TSM just hit fresh all-time highs around ~$330 after a major sell-side catalyst — and the market is treating it like AI demand makes margins immortal.

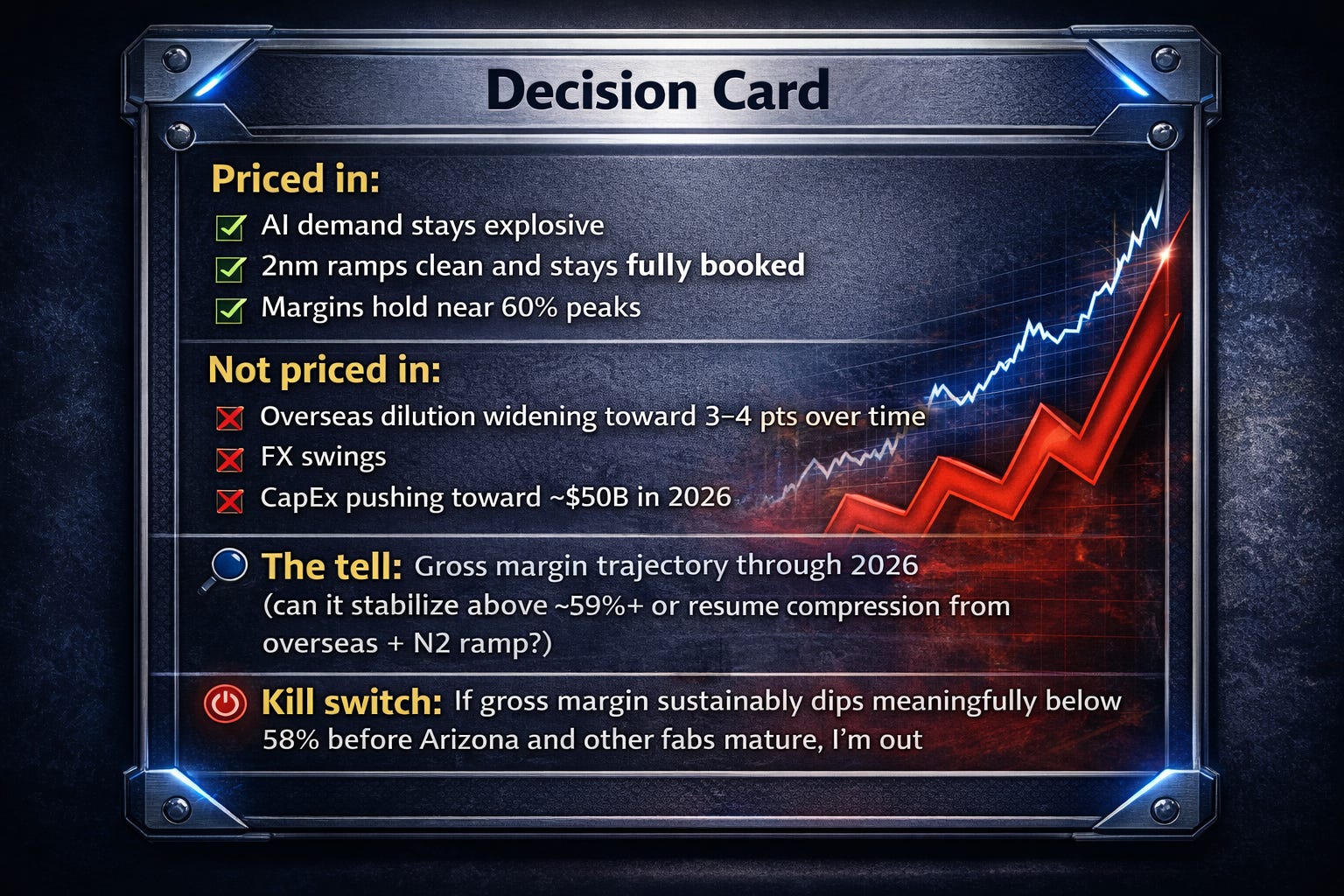

Gross margins are sitting near ~60% in recent quarters (Q3 2025 at 59.5%, Q4 guidance 59–61%). But overseas fabs (Arizona and others) are a structural headwind: management has framed overseas ramps as ~2–3 percentage points of gross margin dilution early, widening toward ~3–4 points later as more offshore capacity comes online.

That’s the mismatch: record highs + premium multiples while the business is openly absorbing a “globalization tax.”

The Call

Thesis: TSM remains the undisputed AI foundry king at today’s price — but at ~33x trailing / ~26x forward, you’re paying full price for flawless execution while the hardest parts of global scaling and new-node ramps are still ahead.

What the Company Actually Does

TSM doesn’t design chips. It manufactures the chips the world can’t live without.

Nvidia, Apple, AMD, Broadcom — they bring the blueprints. TSM turns them into silicon.

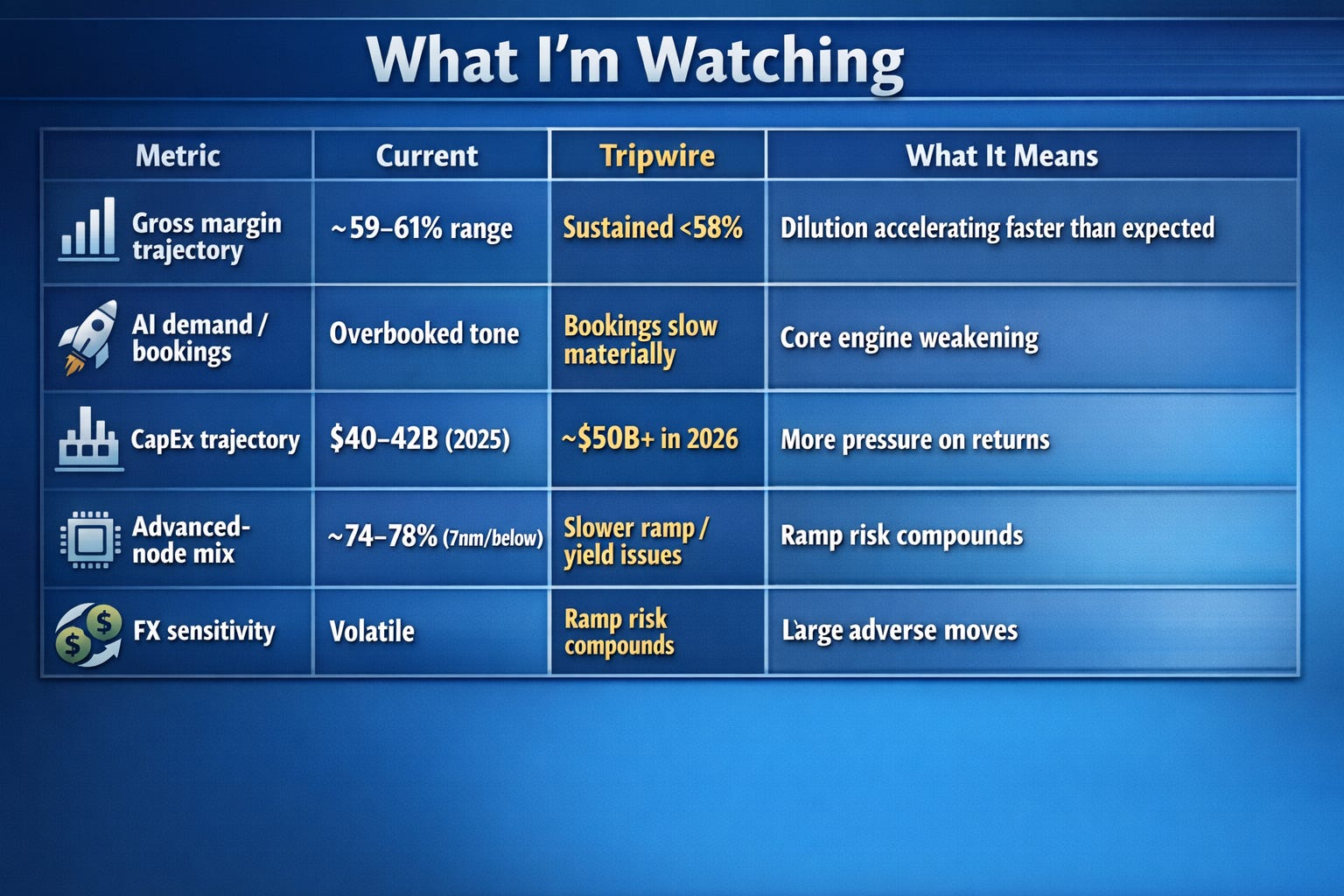

It’s a pure-play foundry: no competing products, no internal designs. Just unmatched capacity and process leadership on the nodes everyone wants most. Advanced technologies (7nm and below) dominate wafer revenue at ~74–78%, with 2nm entering volume production late 2025 and ramping into 2026.

Revenue momentum is real. If you anchor off 2024 and apply the company’s 2025 growth outlook, you land in the ~$115–120B implied range — but the exact number matters less than the reality: AI accelerators are pulling the entire mix forward.

What’s Breaking

TSM is winning the demand war — while margins absorb the cost of winning it.

Overseas dilution is structural — ~2–3 pts early, widening toward ~3–4 pts later as offshore capacity scales

FX volatility is uncontrollable — roughly ~40 bps of gross margin per 1% move in USD/TWD

CapEx stays enormous — ~$40–42B in 2025, with expectations pushing toward ~$50B in 2026 to meet demand

Customer concentration remains real — Apple plus the AI complex drive a large share of growth

New node transitions dilute temporarily — 2nm will pressure averages during early ramp quarters before yields/mix normalize

Price hikes may be needed — but they only stick if demand stays hot enough

The Gap (Consensus vs Reality)

The Street models a plateau. The business model is telling you plateaus cost money now.

Street view: strong growth continues (25–30%+ into 2026), margins stay elevated (~59–61%), AI is the multi-year engine.

My view: growth is real — but structural margin pressure from global expansion and N2 ramp is easy to underestimate. The dilution can last longer and bite harder than consensus wants to admit.

Why it matters: premium multiples assume margins hold. If margins compress faster than growth accelerates, earnings disappoint and the multiple resets.

Where the Returns Came From

The re-rating already happened. Now it’s execution or nothing.

Over the last cycle, a large chunk of the upside came from multiple expansion as the market re-rated TSM into “AI infrastructure.” Earnings growth contributed — but the rerating did the heavy lifting.

Now, with the multiple already elevated versus long-term norms, future returns skew toward:

Earnings growth (volume + mix + pricing), and

Margin durability (whether overseas + N2 dilution stays contained)

Translation: you don’t get paid twice for the same story.

How It Actually Trades (The Machine)

TSM trades like a toll road — until the tolls (margins) start slipping.

Marginal buyer: AI funds, tech ETFs, growth managers treating it as indispensable compute infrastructure

Capital return math: dividend is steady (~1% yield), buybacks are not the core “prop,” and reinvestment dominates

Embedded narrative: pricing power + flawless ramps + margins that defy gravity despite record CapEx

Dependency mapping: a few mega-clients + AI demand cadence

Price mechanics: earnings beats/misses, gross margin guidance, CapEx signals, AI demand updates

Crowding / Ownership: heavily owned — core position for AI exposure

How It Handles News

It rewards clean execution. It punishes cost pressure immediately.

Beats + clean margin guidance = the stock runs.

Any sign of dilution accelerating = pullback risk rises fast.

How It Plays Out

Same company. Two outcomes — decided by margins.

Bull path: AI demand stays tight, 2nm ramps well, pricing sticks, overseas dilution is contained, margins stabilize and later recover.

Bear path: demand softens, costs bite harder, overseas dilution persists, margins compress, FCF lags, multiple contracts.

What It’s Worth (3–5 Years Out)

At this price, you’re buying quality — not margin of safety.

If the AI buildout stays durable and TSM executes, you’ll be fine over 3–5 years. The question is what you’re paying for that certainty.

At ~$325–330, you’re closer to “fair-to-full” than “cheap.”

What the Tape Says

The tape is shouting confidence. The fundamentals are whispering “watch the margin line.”

Near highs after the catalyst run. Strong momentum. Strong narrative.

Who Owns It and Why It Matters

Crowded longs don’t break slowly. They break all at once.

Growth funds, AI thematic investors, major ETFs. If the margin narrative cracks, the unwind can be fast.

How I’d Actually Build the Position

Great business. Full price. Size accordingly.

Starter size: modest (25%)

Add triggers: multiple quarters of margin stability + AI demand holding

Scale rule: size up only when dilution looks like it’s peaking, not worsening

Price Zones (What I Do When)

I don’t chase perfection pricing.

Buy zone: $290–310 on a meaningful pullback with trend intact

Hold zone: $320–360 — monitor execution closely

Trim zone: much higher, if the bull case becomes the only story left

What Would Flip Me

AI demand slowdown

Margins compressing faster/deeper than guided

CapEx ballooning without matching returns

Key client shifts

The Line (Kill Switch)

The story survives. The margins decide the multiple.

If gross margin sustainably falls meaningfully below 58% before global fabs mature, I’m out.

If the stock breaks key support (~$280–290) and holds for weeks, stop adding.

If AI indicators crack materially, sell — the premium multiple depends on it.

Bottom Line

Buy candidate — but not a bargain. Patience is the edge.

TSM sits at the center of AI and advanced computing. Execution track record is elite.

But at ~$325–330, you’re paying for near-perfection while margin headwinds from overseas expansion (measured in percentage points, widening later) and the 2nm ramp sit front and center.

If you own it: hold, watch margins like a hawk.

If you don’t: buy the dip, not the euphoria.

Disclaimer

This content is for informational and educational purposes only — not financial advice. Do your own due diligence before investing. Nothing here is a recommendation to buy or sell any security.

Couldn't agree more, what if that 'globalization tax' on margins expands faster than anticiapted, even with insatiable AI demand?